728 x 90

Advertisement

Here is how blockchain can reduce frauds

- In Techlustre

- 28 Jun 2020

- 9605 Views

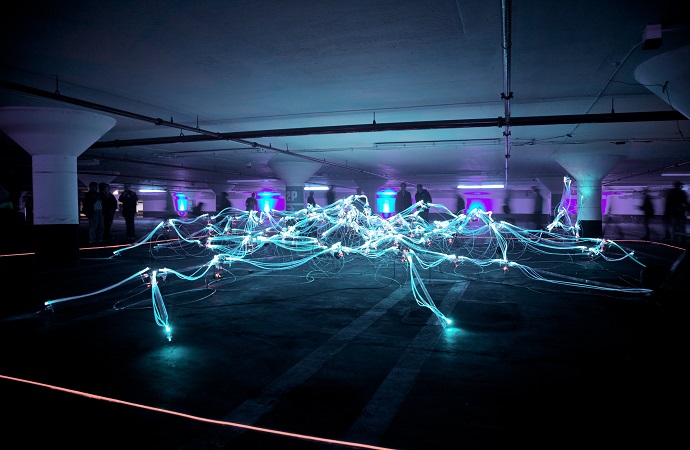

Each and every business working around the world loses at least 7 percent of its revenues to fraud each year. Blockchains are created to prevent internal and external fraudulent attacks in firms. Blockchains provide tight security against tampering, fraud, and cybercrime, and eliminates the replication of human efforts. The blockchain technology is programmed to record all the financial transactions and distributes the information (not copied) digitally. The following are the features of blockchain that helps you from the attack of fraud.

Latest from Techlustre

-

Five Smart TV’s under Rs 30K

- Techlustre

- 16 Jun 2020

-

OPPO A52 Review: OPPO out with A-Powerful phone!

- Techlustre

- 16 Jun 2020

-

Huawei P Smart S Review

- Techlustre

- 14 Jun 2020

-

Mitron Vs Tiktok

- Techlustre

- 14 Jun 2020

-

Shilpa Shetty - Yoga, Fitness, Exercise & Diet App – Review

- Techlustre

- 14 Jun 2020

-

“Lockdown might not affect Tech Industry that much” – Vivek Sharma

- Techlustre

- 03 May 2020

Leave a Comment

Your email address will not be published. Required fields are marked with *

0 Comments

Advertisement

Latest Posts

-

Oh! BUT IT SHOULD NEVER HAVE HAPPENED IN A SCHOOL

- Branwyn

- 22 Aug 2020

-

You must perform your best : Gaurav Sharma Lakhi

- Branwyn

- 28 Jul 2020

-

How Chris Pratt Landed The Role Of Star-Lord?

- Reel Life

- 02 Jul 2020

-

Tips to Manage Stress in the Times of Pandemic

- Shots

- 02 Jul 2020

-

Five Reasons Why Startup Ventures are Important for India

- Moneywise

- 02 Jul 2020

-

Here is how Businesses Use Social Media for Maximum Profit

- Moneywise

- 02 Jul 2020

-

आत्मनिर्भर भारत बनाम विकासदूत

- अनुकृति

- 01 Jul 2020

-

Top 5 Richest Writers in the World: 2020

- Branwyn

- 30 Jun 2020